With Bonds Paying Next to Nothing, Should We Bother Owning Them Today?

With bond yields at such low levels, Investment Committees are questioning the role of bonds in their portfolios—and rightly so. Today’s bond market is not what it used to be. Seemingly insurmountable headwinds continue to weigh on returns and expected yields are meager at best. With interest rates at levels that appear to have nowhere to go but up, further pressuring returns, why should we own bonds today?

Our response to most investors with spending objectives, long-term time horizons, and broadly diversified portfolios, is that bonds still have a useful place in their overall asset allocation strategy. Before we explain why, let us briefly look at the headwinds facing the bond markets today.

Challenges Facing Today’s Bond Investors

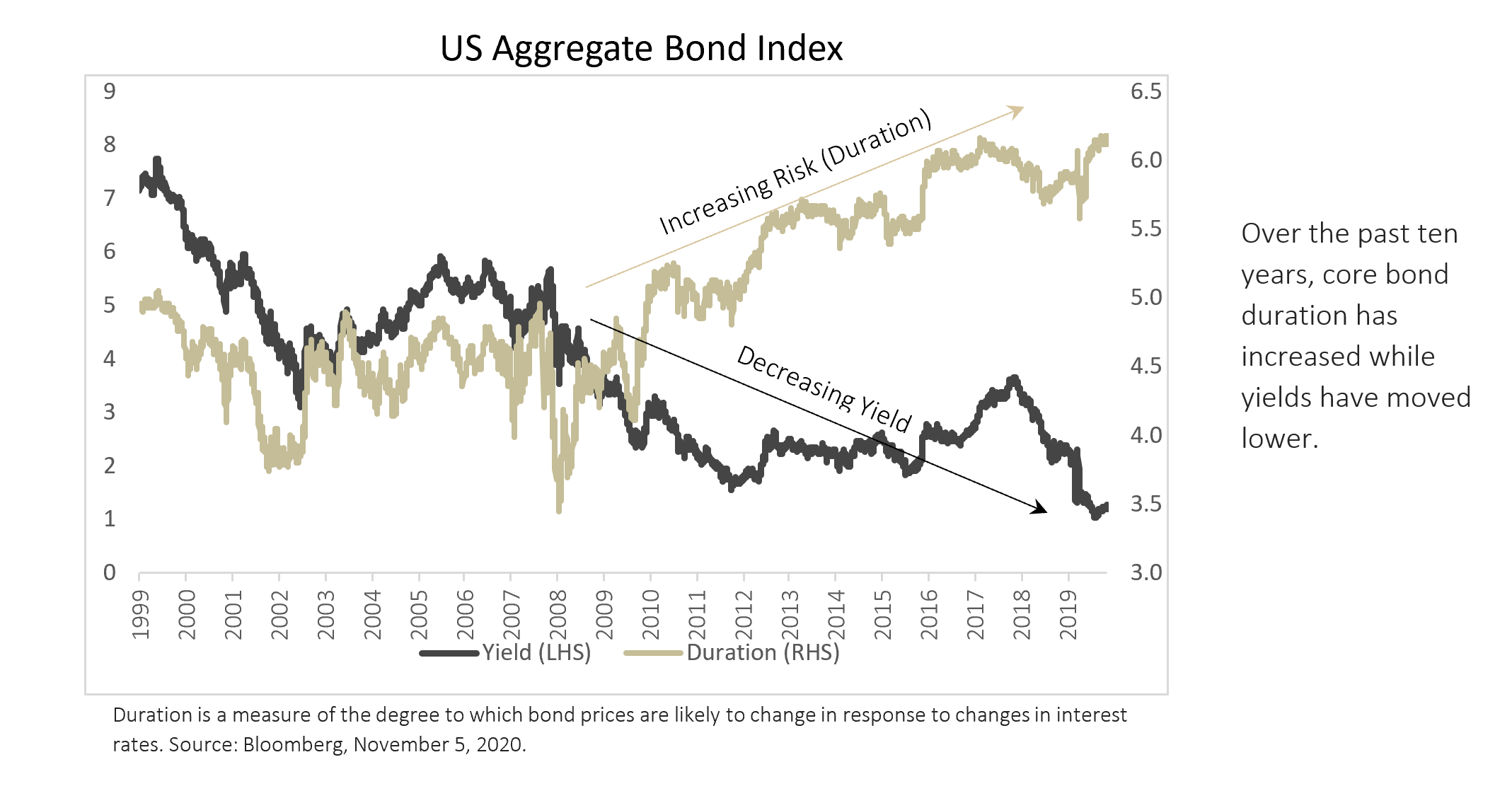

The global fiscal response to the pandemic in 2020 was unprecedented. Stimulus and market support came swiftly and at a level markets had not seen before. The resulting decline in yields across bond markets—yields, by the way, that were already at historic lows before the pandemic—has left investors facing an environment of paltry expected returns going forward. Pair that with the increasing sensitivity to rising interest rates (measured by duration) and you have an unpleasant conundrum: more risk for less return on what should be your portfolio’s safety net.

The Role of Bonds in a Total Return-oriented Portfolio: Stability, Diversification, Downside Protection

Given the current market environment, it is prudent to go back to the bigger picture of the role that bonds play in a total return-oriented portfolio. Fiduciaries guided by UPMIFA standards are required to view holdings in context of the portfolio as a whole, not in isolation. And much of language in the UPMIFA standards is driven by Modern Portfolio Theory—the idea of combining asset classes that do not act the same at a given time (i.e., uncorrelated or negatively correlated) to improve portfolio outcomes by increasing returns or reducing risk.

Bonds have historically been an obvious choice for investors when looking for a stabilizing influence to manage portfolio risk. The volatility of bonds has been much less than stocks and until most recently, a modest return could be earned to boost overall returns and support spending.

Additionally, investors can achieve diversification benefits from the relationship of returns between stocks and bonds. Core bonds have historically been negatively correlated to stocks.* Roughly, this relationship has meant that when one asset class goes down, the other moves up. The obvious benefits of this relationship are not experienced during equity-oriented bull markets when bonds are a drag on overall return, but is rather more noticeable when the stock market has gone down and bonds have maintained their value.

During equity bear markets, having some exposure to fixed income can help in two major ways: 1) Portfolios are down less, thus minimizing permanent impairment when liquidating the portfolio to support necessary spending, and 2) by losing less, it takes less time to recover the full value of the portfolio when markets rebound, especially when rebalancing between asset classes. For community foundations with spending objectives, this can be especially beneficial as the demand for increased spending in the community often coincides with a struggling stock market.

But is this time different?

There is no crystal ball that tells us the best way to invest. We cannot know if, when, how, or how much interest rates will rise in the short-term. As fiduciaries, we are not expected to time the markets or be right about every short-term decision in the portfolio. While we are tasked with the responsibility of considering current market conditions, the focus of our attention should be on setting a long-term strategy and maintaining a disciplined approach in executing that strategy.

The basic nature of a bond is unchanged—lending capital to a qualified borrower and receiving repayment of that capital plus interest over time. This still suggests that it is a more conservative investment choice compared to equities or other asset classes and should continue to provide relative stability, diversification benefits, and downside protection in the long run.

What should we be doing today?

Here are some methods investors might consider to mitigate the near-term challenges of fixed income in their portfolios.

Consider Active Management

Active managers do not have to take the current interest rate environment “lying down.” By managing duration, they can structure their portfolios in ways that can provide some protection in the event of rising rates. Also, through sector selection they can boost return potential by investing differently than the Treasury-heavy Barclay’s Aggregate Index. Additionally, they can add value through successful security selection, yield-curve management, and in several other ways. Most importantly, active managers are constantly scrutinizing the bond markets searching for opportunities, and monitoring for unexpected risks.

Consider Broadening the Fixed Income Universe

Bond managers with the latitude to invest in sectors beyond the Aggregate Index have a greater opportunity set at their disposal for adding value. Sectors like Floating-Rate Notes, TIPS, High Yield, International, and Emerging Markets Debt all have unique characteristics that can potentially add value to a fixed income portfolio and mitigate some exposure to rising rates. These sectors also have different, and sometimes greater risks than traditional core fixed income sectors which need to be carefully considered before investing.

Revisit the Portfolio Asset Allocation

While we have discussed the benefits of holding bonds, investors today would be wise to evaluate their overall asset allocation strategy, including the tradeoff between the downside protection they desire and long-term expected returns they need. When reviewing asset allocation in the context of fixed income, the question becomes this: If we reduce our fixed income exposure in the portfolio, where will we allocate that capital instead?

Equities are a more volatile alternative to bonds, and while they may boost expected returns over time, the tradeoff is more short-term risk and thus less downside protection. Furthermore, equities, particularly large cap U.S. stocks, are facing their own set of headwinds as investors have enjoyed more than a decade of double-digit annualized returns (measured by the S&P 500). The general consensus for equities going forward is much lower in terms of expected return, while expected risk (volatility) continues to be high.

Some investors have looked to alternative assets to replace a portion of their bond allocation. Institutional investors have increasingly turned to alternatives, particularly strategies that attempt to provide bond-like diversification benefits versus stocks, but with potentially higher returns than bonds. The drawback has been that while many alternative strategies have promised downside protection as a replacement to bonds, history has shown that only some have been able to consistently deliver when it counted. Other characteristics of alternatives, like illiquidity and fees, make them less appealing than bonds for providing liquidity and efficient rebalancing.**

Unfortunately, there is no easy answer for Investment Committees in today’s environment—especially when it comes to bonds. We believe that fixed income still has an important role in a diversified portfolio by providing stability, diversification benefits, and downside protection. We also believe that actively managed fixed income strategies and broadening the fixed income opportunity set can offer benefits to a portfolio in today’s environment. The best solution for investors is the one that is made after evaluating all potential benefits and considerations and is executed over long periods of time.

FOOTNOTES:

*Over the last 10-year period, ending 2/28/2021, correlation between the S&P 500 and the Barclays Aggregate Index is -0.1

**Additional risks that are inherent in the alternative investments should be understood before investing.

About the Authors

Janet S. Sweet, CFA, CAIA – Institutional Investment Advisor

Janet S. Sweet serves in the role of Institutional Investment Advisor, responsible for providing our growing institutional client base with consultative advice and high quality service. Janet brings over 25 years of industry experience to Goelzer. Previously, Janet has advised institutional clients on the development of customized asset allocation studies, investment policy statements, performance attribution , as well as manage due diligence and evaluation. Janet earned a B.S. degree with a major in Financial Counseling and Planning from Purdue University. Janet has also earned both the CFA and CAIA credentials. Janet serves as Board Member and Finance Committee Chair of the Dove Recovery House for Women.

Gavin W. Stephens, CFA – Director of Portfolio Management

Gavin W. Stephens serves in the role of Director of Portfolio Management, responsible for leading the firm’s portfolio-management and trading processes. In addition, Gavin serves as a lead fixed-income portfolio manager and as a member of the firm’s Investment Policy Committee. Gavin’s responsibilities include developing fixed-income strategy for taxable and tax-exempt bond strategies and actively managing the firm’s fixed-income portfolios. Prior to joining Goelzer in 2014, Gavin worked in the academic publishing field, serving in a number of roles, including as a member of the executive leadership team. Gavin earned a B.A. degree with a major in Theological Studies from Hanover College. He also holds an MTS from Harvard Divinity School, an MBA from the University of Louisville, and is a CFA Charterholder. Gavin serves as Board Member for the Cystic Fibrosis Foundation, Indiana Chapter and is member of the endowment committee of Trinity Episcopal Church.

The information provided in this material should not be considered as a recommendation to buy, sell, or hold any particular security. This report includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions, or forecasts will prove to be correct. Actual results may differ materially from those we anticipate. The views and strategies described in the piece may not be suitable to all readers and are subject to change without notice. You should not place undue reliance on forward-looking statements, which are current as of the date of this report. The information is not intended to provide and should not be relied on for accounting, legal, and tax advice, or investment recommendations. Investing in stocks involves risk, including loss of principal. Past performance is not a guarantee of future results.